Can Bitcoin cross the Rubicon?

Hatchworks has prepared a report on Bitcoin, introducing a framework known as The Grid, to assist institutional investors in better understanding Bitcoin’s place in the broader asset landscape now and in the future.

In context of the systemic shock our global economy has faced owing to the pandemic, ongoing debasing of fiat currencies and global debt levels have reached all-time-highs in 2020. As a result we believe systemic stress has increased. Central banks continue to ease and in major stock markets such as the U.S, the S&P and other parts of the stock market have received direct liquidity injections by the Fed contributing to a historical earnings gap between valuations and corporate earnings.

With valuations bubbling across many asset classes such as equities and in certain classes of debt, coupled with increasing demand for inflation protected safe havens, it is no surprise that Bitcoin’s price has climbed over 130% this year, nearing its all-time-highs of 2017 where it reached $20,000.

While Bitcoin’s market valuation of $330bn may seem lofty, we run scenario analyses in this report that showcase how this can change over the coming years, if other global assets are benchmark to go by.

The Grid

We have constructed ‘The Grid’ below, which scores Bitcoin relative to other major global assets, on what we believe are thirteen key value drivers. For each driver where the asset in question meets the criteria, it receives a ‘Yes’ and a score of 1, with a total possible score of 13.

Bitcoin’s supply is fixed and release schedule, cryptographically audited. Its supply is finite and is starting to be regarded as an institutional store of value as billion-dollar corporations such as Square, Microstrategy, Fidelity and others, have begun building large positions or plan to offer investment services for it. Interestingly, major regulated venues have even created lending markets based on Bitcoin which allow it to yield. Relatively speaking, transaction costs for sending Bitcoin are low and the process of sending it, quick. Yet, Bitcoin is still in its infancy as The Grid shows.

Namely, its supply is not entirely secure with concerns surrounding the fact that large mining pools are concentrated in China and that the network is not impervious to 51% attacks. As it’s digital, it has no physical utility. Bitcoin broadly is not regarded as a payment mechanism (yet) and regulators are still working on understanding how incorporate it into a broader global KYC/AML framework, given its decentralised nature. Last but not least, it is substitutable and not backed by any assets. For these reasons, The Grid scores Bitcoin a 5.5/13, a 25% structural discount to the average score of peers. We view this discount as a potential opportunity, should the Bitcoin network continue to address some of its weaknesses and society continues progress along the adoption curve.

While hurdles such as lack of physical utility cannot be overcome, the security of bitcoin’s supply (read nodes), we believe, can improve as the number of nodes powering the network grow and do so in a more geographically disperse manner. This process, however, is likely to play out slowly over the coming decade and would need larger, notable institutions to invest in capacity thereby bringing a veneer of credibility to the supply base.

As for Bitcoin’s lack of buying power, while this is partially explained by it being regarded as a store of value/chaos-hedge, as opposed to a payment mechanism, the main reason behind weakness on this front is its lack of merchant integration and major payment-service-providers not having adopted it in any meaningful manner, until recently. Fortunately, this has started to change with PayPal recently on-boarding Bitcoin and major retailers such as Whole Foods, Starbucks and more accepting Bitcoin payments. In our opinion, we see no reason why this trend will not percolate through other sectors as well. This brings us to regulation. The case for future bans on bitcoin are there, but the balance of probabilities, in our view, indicates that if major payment networks and corporations are on-boarding Bitcoin, it is likely they will use their political lobbying muscle to help regulations move in the right direction.

Coming back to The Grid; if Bitcoin is able to overcome these barriers then it would score above 8/13, if not higher, thereby possibly establishing itself alongside other assets (e.g. Gold, cash, equities), over the coming years. This may have resulting ramifications on its valuation, but is by no means a guarantee.

Real Estate, which is by all parameters the highest valued asset, clocking in at c. $280 trillion, also happens to score the highest on The Grid with a score of 9/13. It has most value drivers in that its supply is audited (national land registries), secure, finite, has physical utility (that cannot be substituted unless humans plan a mass relocation to jungles), is regulated, widely regarded as a store of value and yields (via rental income). It, however, doesn’t have direct purchasing power, nor can applications and entire industries be built on it (beyond mortgages and the real-estate agency space). Additionally, transacting in real-estate is slow and costly.

Bitcoin has often been compared with gold; either as another possible store of value or as a digital successor. Unlike maximalists, we do not see Bitcoin replacing gold, but can see it taking some share in the future. Gold’s value clocks in at around $16 trillion and as its supply is audited, secure, broadly regulated, finite and like it or not, over half of its value is backed by real physical utility (c. 49% comes from ornamental value and c. 7.5% from actual use in industrial production), it scores relatively well on The Grid with a 7/13.

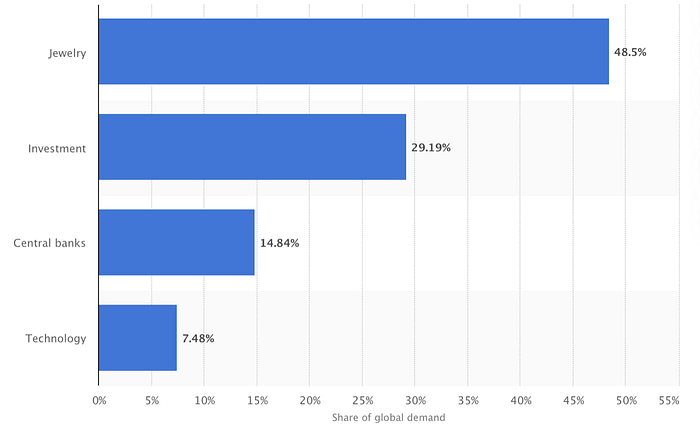

While gold has no direct buying power nor does it yield, it is widely perceived as a store of value; so much so that central banks account for almost 15% of global gold demand and c. 30% comes from speculative investing. While the jury remains out on whether or not central bank demand could increase for Bitcoin, what is certainly possible is speculative demand that currently views gold as a store of value, shifting its focus and diversifying into Bitcoin.

Cash gets a bad rap mainly for being inflationary and infinitely printable by central banks. Yet, cash still is king with it having an audited supply, one that is secured (i.e. not powered with nodes in Dave’s proverbial basement), has immense direct buying power for goods and services, is a store of value with relatively low volatility albeit declining purchasing power parity, is regulated and yields in normal economic conditions. Its transaction costs are extremely low and speed, high. For these and other reasons, cash receives a score of 8.5/13 on The Grid and has an approximate value of $96 trillion.

Bitcoin has certain advantages over cash in that it cannot be inflated and while it is seen as a store of value like gold, unlike the yellow metal, however, it can also be used to transmit value from one party to another within minutes. This is why payment processors are integrating Bitcoin and not gold.

We view Bitcoins’ journey in the coming years with cautious optimism and believe that, on balance, it may overcome some if not all of its current barriers highlighted in this report. This is because security of supply, regulations and the ability to pay for goods and services with Bitcoin are not insurmountable obstacles. Where exactly it lands in terms of valuation, relative to other major assets, depends on how successful it is in overcoming these barriers and thereby increasing its score on The Grid.

The Grid provides investors with implied Bitcoin valuation reference points (not price targets) which show where a theoretical valuation range could lie, in the event Bitcoin’s score on The Grid moves up or down. For example, if in the long run the market perceives bitcoin as an inflation/chaos hedge, but also uses it for perhaps, larger transactions, thus giving it buying power similar to cash, then could it value Bitcoin at somewhere between Gold and Cash? For then it would have crossed the rubicon.

Risks

There are structural risks that give us cause for concern and some of these have been highlighted already. These are:

Supply: There is a concentration of node supply at large mining pools in China. Concentration increases 51% attack risk. Chinese firms Bitmain, Microbt, Ebang, and Canaan manufacture a disproportionately large amount of global mining rigs. Amongst these outlets, Bitmain has a wide margin of dominance over other players. Production disruptions, state seizures or force majeure can result in supply-side shocks. Additionally, Bitcoin miners are energy intensive with a carbon footprint. The optics of running large farms of miners in an increasingly environmentally conscious world along with the negative impact of high energy consuming machines on miner-ROI, could result in slow node growth.

Regulation: In the previous cryptocurrency boom, banks and central banks had taken aim at Bitcoin, however since then there has been a more accommodative stance towards the sector. Central banks enjoy control over money and Bitcoin by design cannot be printed ad nauseam, nor can it be controlled per se. Should Bitcoin’s dominance grow, it may pose a systemic risk to central bank power resulting in adverse outcomes for the digital asset.

Scalability: Bitcoin blocks record transactions on the network. Generally speaking, processing capacity of the network is limited by the average block creation time of 10 minutes and the block size limit of 1MB. Despite solutions being worked on to address these issues (eg. Layer 2), these impediments restrict scaling and if not addressed in time, can limit adoption or ring-fence Bitcoin’s use-case in the future.

Substitutability: AltaVista was the most popular search engine when the internet was dawning in the mid 90s. They famously turned down proposals by a tiny startup called ‘BackRub’ (today known as Google) to buy them out for their technology for a price tag of c. $1m. Fast forward 25 years and Alphabet (Google) is worth over a trillion USD. Bitcoin may be the dominant force now, but this does not mean it will necessarily retain its dominance forever. This is a known unknown.

Technology: A known ‘known’ attack vector on the integrity of the Bitcoin network is/are quantum computers that use the concept of quantum entanglement to process computations millions (if not billions) of times quicker than current high power computers. A recent study by Deloitte demonstrated that around 20–25% of Bitcoin wallets that either show un-hashed public keys (thus allowing user’s private keys to be decrypted) or re-used wallets are susceptible for a quantum hack in the future. This would severely compromise the integrity of the network and more importantly, perceived security.

That being said, quantum computers can in theory be used to hack and decrypt major encryption protocols across various industries and therefore in order to thwart this, superior encryption methods are being developed that are ‘quantum proof’ and hack resistant to this vector. It will be a major responsibility, in our view, for Bitcoin Core (the team behind Bitcoin), to ensure the encryption routines are updated and adopted by miners, to ensure the network’s security increases apace with upgrades to computing technologies.

The Hatchworks Team

Disclosure: Hatchworks is an investor in a range of equities, gold, bonds, bitcoin and other assets on a proprietary basis. The information provided in this document is not investment advice nor is it a solicitation to invest in any asset. For webinar, social media appearances or a pdf copy of this report, you may send an email to info@hatchworksvc.com.